Some Good News…

Some Good News…

Dips are being bought and that’s the game plan for the foreseeable future.

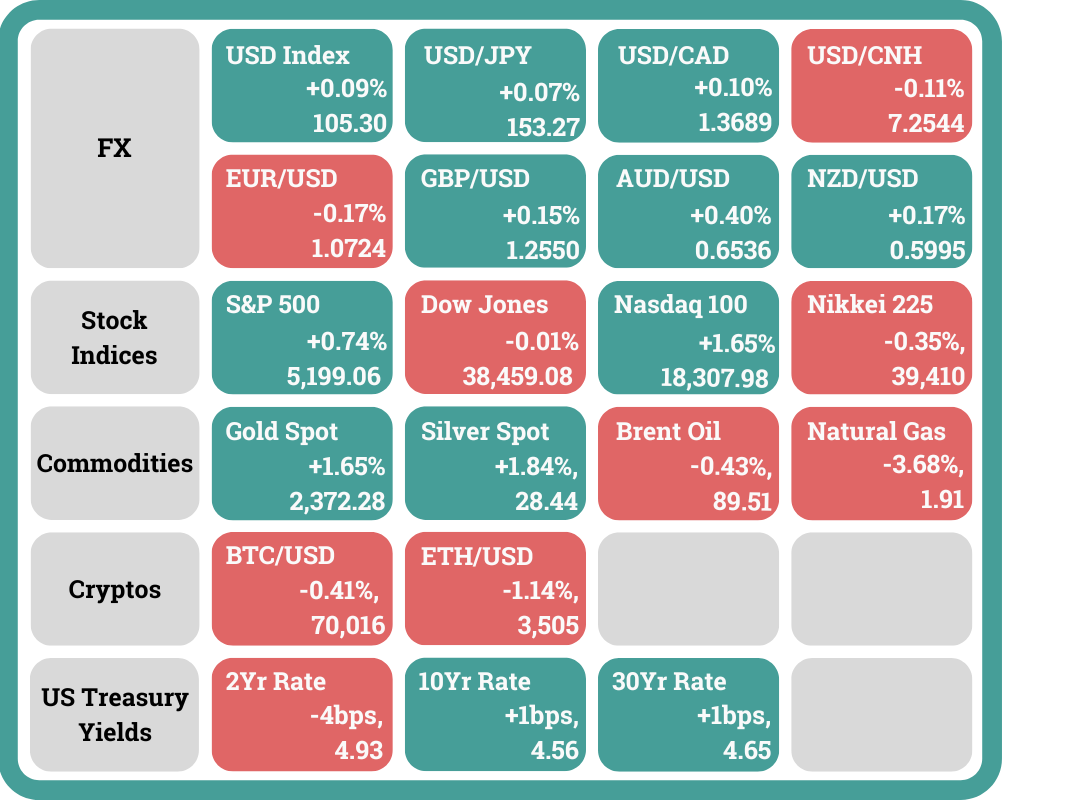

After the upside surprise in the US Consumer Price Index inflation data yesterday (+3.5% vs expected +3.4% and previous +3.2%), the market was bracing itself for more bad news from the Producer Price Index data. However, headline PPI surprised to the downside (actual +2.1% vs expected +2.2% and previous +1.6%).

The downside surprise was a relief to the market and boosted stocks with S&P 500 rising 0.74% and Nasdaq rallying strongly to close 1.65% higher. Also, Fed official, Williams, said that the disappointing inflation setbacks recently are not a surprise to the Fed. This means that the median projections of 3 interest rate cuts this year incorporates disappointment on the inflation data front. This is consistent with what Fed Chair Powell said in his post-meeting press conference in March that inflation is headed lower but the path will be bumpy.

The price action in stocks is telling. Dips are being bought and that’s the game plan for the foreseeable future.

Trading Tip

Set Your Risk Limits Clearly

Defining your risk is important in life endeavours as well as in trading. You need to know how much you are risking before you enter a trade. By setting these boundaries upfront, you can manage potential losses proactively, ensuring they remain within a level you're comfortable with.

This practice not only helps in maintaining peace of mind but also prevents you from making impulsive decisions driven by emotions. After all, your greatest asset as a trader is your mental clarity and the only way to maintain it is to ensure that you are in a good psychological state.

Day Ahead

The preliminary data for the US University of Michigan Consumer data will be released. The Inflation expectations components will be the focus.

Trading Plan

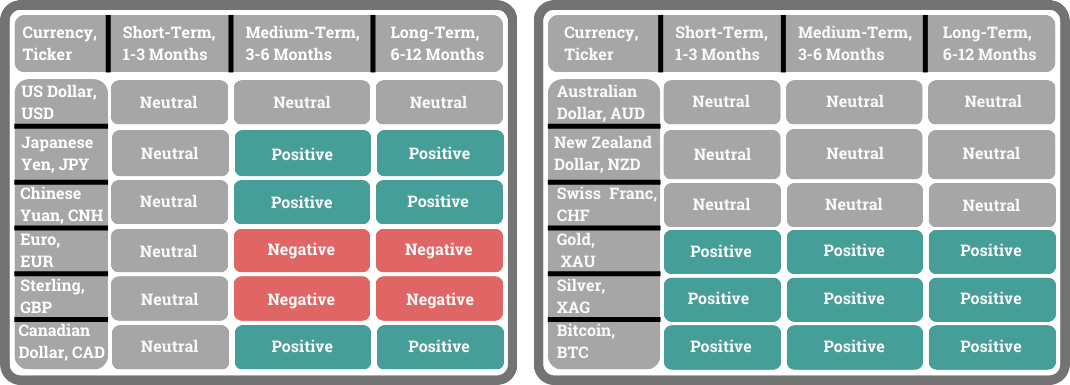

1. Currencies:

Neutral

2. Commodities:

Uranium & Energy - Stay invested for now.

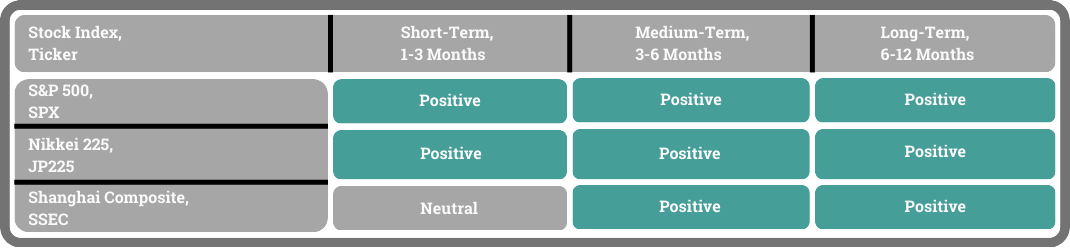

3. Stocks:

US Stock Index: The S&P 500 (+0.74%) and Nasdaq 100 (+1.65%) managed to rise on the day as the headline US PPI print came in slightly softer than expected. Nasdaq was also boosted by gains in Apple (+4.33%), Nvidia (+4.11%) and Amazon (+1.67%). The Dow Jones Index saw a miniscule loss of -0.01%.

(For more timely info on our Trading plan, click HERE)

Single Stocks: TrackRecord Model Portfolio is tracking the broader market for now.

Key risks: Comments from Fed officials about their views on the possibility of interest rate cuts in the months ahead could influence risk sentiment.

What Happened Yesterday

Fedspeak:

Williams (current voter, known centrist): “No need to change monetary policy in the very near term.” "Recent inflation setbacks are not a surprise to the Fed." "Fed forecasts rate cuts starting this year."

Barkin (current voter, slight hawk): "Inflation data did not increase my confidence that disinflation was spreading." "Fed is not yet where we want to be on inflation, though headed in the right direction over a longer time frame."

(Williams is becoming neutral from a more dovish stance previously. Barkin is moderating from his previous opinion that disinflation is likely to continue.)The European Central Bank (ECB) kept its interest rates unchanged at a 22-year peak of 4.5% for the fifth time in a row during its April meeting. The ECB hinted that it might lower these high rates if it becomes more confident that inflation is heading towards its 2% goal. They noted that inflation has been falling, with both underlying inflation and wage growth slowing down. However, they warned that prices within the economy are still rising, particularly in services. ECB President Lagarde emphasised in a press conference that the ECB hasn't committed to any specific future rate changes, indicating that any decisions will be data dependent. Reaction in the EURUSD was muted.

The US Producer Price Index (PPI) showed that prices rose +2.1% Year-on-Year (vs +2.2% expected) in March 2024, marking the highest increase since April 2023. This was a rise from the +1.6% increase in February. Core producer prices, which do not include food and energy costs, rose +2.4% YoY (vs +2.3% expected), up from +2.1% the previous month (revised from +2%). On a monthly basis, overall producer prices in March saw a modest increase of +0.2% (vs +0.3% expected), the smallest in three months. Similarly, core producer prices also rose by +0.2% MoM as expected, following a +0.3% increase in February. The US 10 year yield fell -0.05% from 4.58% to 4.53% while the S&P 500 futures spiked +0.63% in immediate reaction. After yesterday’s upside surprise in CPI, investors were expecting a bad PPI, but with the headline PPI index printing below expectations, risk sentiment was boosted.

The US Treasury Yield curve inversion narrowed to 0.37% as the US 2-year bond yield slipped -0.04% to 4.93% while the 10-year yield edged +0.01% higher to 4.56%.

The US stock futures traded within a range during the Asian trading hours. However, the S&P 500 futures started to edge lower through the London trading session and fell -0.43% just before the US PPI data was released. The softer than expected headline PPI then caused the S&P 500 futures to bounce +0.63% from the lows.

The US stock market opened higher from Wednesday. It then experienced a slight pullback in the early New York session before rising higher through the rest of the day. The S&P 500 finished +0.74% higher (high: +0.99%, low: -0.42%), the Dow Jones edged -0.01% lower (high: +0.36%, low: -0.69%) while the Nasdaq climbed +1.65% (high: +1.81%, low: -0.07%).

Apple (Nasdaq: AAPL) rose +4.33% on the day as Bloomberg reported an overhaul to its Mac line with AI-centred M4 chips. Nvidia (Nasdaq: NVDA) also saw a +4.11% rise on the day. Amazon.com (Nasdaq: AMZN) rose +1.67% as CEO Andy Jassy announced in a shareholder letter that the company is committed to cut costs while investing in AI.

The crypto market remained in a range despite the rise in US stocks. BTC (-0.41%) and ETH (-1.14%) were down slightly despite the stronger risk sentiment.

Headlines & Market Impact

Fed can start cutting interest rates by end of 2024, IMF managing director says

Notable Snippet: The Federal Reserve should be able to start cutting interest rates by the end of 2024, according to Kristalina Georgieva, managing director of the International Monetary Fund.

“We remain on our projection that we would see, by the end of the year, the Fed being in a position to take some action in a direction of bringing interest rates down,” Georgieva said on CNBC’s “Squawk on the Street.” “But again, don’t hurry until the data tells you you can do it.”

Georgieva said the Fed should continue following economic data, which will signal when it’s appropriate to begin reducing the cost of borrowing money.

People should be optimistic about the future of the United States as the country does not feel as much upward pressure on labour costs compared with other places, the former World Bank CEO said. And the U.S. government can play a relatively bigger role in keeping the economy from overheating, Georgieva said, which is another reason for optimism on the country’s financial health.

Still, Georgieva warned that keeping interest rates elevated for longer than expected can create risks to financial stability for the rest of the world. Meanwhile, she said central banks around the world will be less likely to follow the direction of the U.S. Fed as conditions diverge.

“Inflation is going down,” Georgieva said. “But, it is not yet where we want it to be.”

What we think: Whether the Fed cuts or not and when they begin so will depend entirely on data.

Goldman still expects U.S. inflation to fall significantly as markets alarmed by recent rise

Notable Snippet: In the Goldman Sachs view, the U.S. CPI will fall back to 2.4% this year, down from the current annualised rate of 3.5%.

“The problem is that you have certain parts of the inflation bucket right now that are continuing to push things up,” Christian Mueller-Glissmann, head of asset allocation research at Goldman Sachs, told CNBC’s “Street Signs Europe” on Thursday.

“In the last print, it was the transportation. We obviously have oil prices currently going up, and that’s certainly something that has been a bit stronger than what we initially anticipated,” Mueller-Glissmann said.

He added that the inflationary impact of rising oil prices will likely be limited, because the bank expects that OPEC will eventually bring spare capacity online.

Mueller-Glissmann said that the normalisation of wage inflation was one of the core reasons why Goldman expects U.S. inflation to fall. On this point, he conceded that there were “more question marks” for the U.S. compared with Europe, when it comes to wage normalisation.

“But we would still argue that a lot of the higher frequency indicators of job openings, for example, in the U.S., are coming down. So, the labour market is still cooling so one would hope that would let wage inflation ease a bit.”

What we think: If Goldman is right about inflation, it is likely that the Fed will start cutting interest rates before then.

ECB cannot ignore Fed as it goes down its rate cut path

Notable Snippet: The European Central Bank may protest it is not "Fed-dependent" but it will likely find itself singing from a hymn sheet largely written by the U.S. Federal Reserve whether it wants to or not.

The ECB is sticking to plans to reduce interest rates from record highs, likely at its next meeting in June, in light of a continued fall in inflation in the 20 countries that share the euro.

This is in contrast to U.S. price growth, which has beaten analyst expectations for three months straight, and is now expected to keep the Fed from lowering its own borrowing costs until September.

ECB President Christine Lagarde insisted her institution was "data-dependent, not Fed-dependent" on Thursday. But analysts and policymakers said high U.S. inflation and interest rates were bound to have an impact on the ECB's plans via financial markets and trade.

"While we continue to believe that the ECB will be the first central bank to start cutting rates this year, the path beyond that will remain dictated by Fed action," Max Stainton, a senior global macro strategist at Fidelity International, said.

What we think: Euro inflation is currently at the 2.4% level and it has been showing a downtrend for the past three months. If this should continue, the ECB will have greater confidence to begin its interest rate cuts.

Sentiment

FX

Stock Indices

Best,

Phan Vee Leung

CIO & Founder, TrackRecord