When will we see interest rate cuts?

When will we see interest rate cuts?

As such, there is no need to jump to conclusions or pretend to know when the cuts will come.

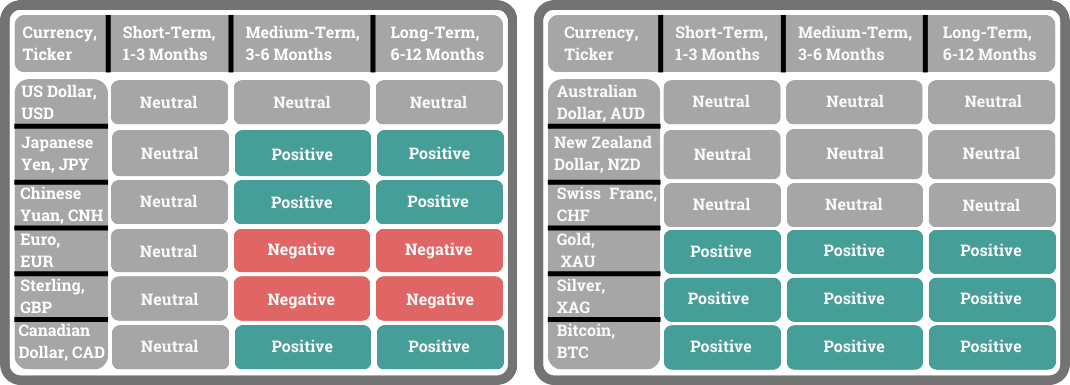

According to the US Federal Reserve Chair Powell, it is taking “longer than expected to achieve the confidence” to start cutting interest rates. The European Central Bank President Lagarde, on the other hand, said that barring any additional shock, “it will be time to moderate the restrictive monetary policy in reasonably short order”.

Why are their views diverging? It’s all about the data. Inflation data in the US have been surprising to the upside while in Europe, it’s been surprising to the downside and continuing to moderate lower. This is what the policymakers have been telling us too.

They are highly data-dependent and will only cut interest rates when the data gives them the confidence that they’re not prematurely rushing to cut. As such, there is no need to jump to conclusions or pretend to know when the cuts will come. It’s all about the data and no one has been a great predictor of inflation in the last few years. So till there is more clarity, keep an open mind and wait for the confirmation because when the rate cut starts, it will not be too late to jump on the bandwagon.

Trading Tip

Be Unbreakable

Success in trading often requires more than just skill and knowledge. It demands resilience. Many successful traders have faced substantial financial setbacks and the mental and emotional challenges that come with frequent losses. The journey to becoming proficient can be fraught with challenges that test your endurance and adaptability.

It's crucial to view these setbacks as integral parts of the learning process. By persevering through tough times, you learn invaluable lessons that refine your strategies and strengthen your approach. Stay committed, learn continuously, and use your experiences, both good and bad, as stepping stones to achieve lasting success in trading.

Day Ahead

The Euro Area Inflation is expected to show that prices rose +2.4% Year-on-Year in Mar, down from +2.6% in Feb. The core rate is expected to come in at +2.9% in Mar, down from +3.1% in Feb.

Inflation data from the UK in terms of Consumer Price Index (+3.1% exp vs +3.4% prev, core: +4.1% vs +4.5% prev).

Trading Plan

1. Currencies:

Neutral

2. Commodities:

Uranium & Energy - Stay invested for now.

3. Stocks:

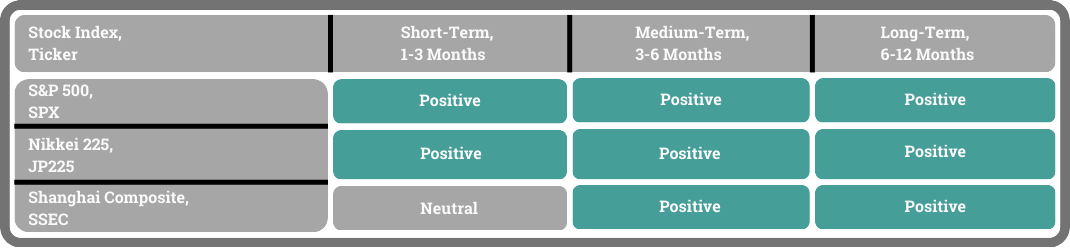

US Stock Index: The US Stock market traded within a range yesterday with the market already pricing in the lower likelihood of three interest rate cuts happening this year despite Powell’s speech.

(For more timely info on our Trading plan, click HERE)

Single Stocks: TrackRecord Model Portfolio is tracking the broader market for now.

Key risks: Comments from Fed officials about their views on the possibility of interest rate cuts in the months ahead could influence risk sentiment.

What Happened Yesterday

Fedspeak:

Powell (Chair, known centrist): “The recent data have clearly not given us greater confidence and instead indicate that it’s likely to take longer than expected to achieve that confidence.”

Jefferson (current voter, known centrist): “It will be appropriate to hold in place the current restrictive stance of policy for longer.” "My baseline outlook continues to be that inflation will decline further, with the policy rate held steady at its current level, and that the labour market will remain strong, with labour demand and supply continuing to rebalance."

Williams (current voter, known centrist): “Inflation has fallen across all categories over the last year and a half.”

(Powell is delaying his expectation for the start of interest rate cuts given the data we have seen thus far. Jefferson remains data dependent, adjusting his view based on recent data. Williams’ focus remains on falling inflation. )

Although Powell is changing his expectation for the start of interest rate cuts because it’s taking “longer than expected to achieve” the confidence that inflation is headed towards the 2% target, the market reaction was relatively tame given that interest rate futures were already pricing for the delay. The probability of the first cut coming in June, which was more than 50% a week ago, had already dropped to just 20% the day before. The odds dropped further yesterday to 15%.

Canada's annual inflation rate slightly increased to +2.9% in March as expected from the eight-month low of +2.8% in February, aligning closely with the Bank of Canada's prediction of around +3% for the first half of the year. However, other key inflation measures watched by the Bank of Canada showed a slower increase than anticipated: the trimmed mean inflation slowed to +3.1% (previous and expected +3.2%), and the median rate decreased to +2.8% (previous and expected +3.0%). Additionally, the annual core inflation, which excludes volatile items, dropped to +2% in March, marking its lowest point since March 2021. The USDCAD pair spiked up +0.28% in immediate reaction.

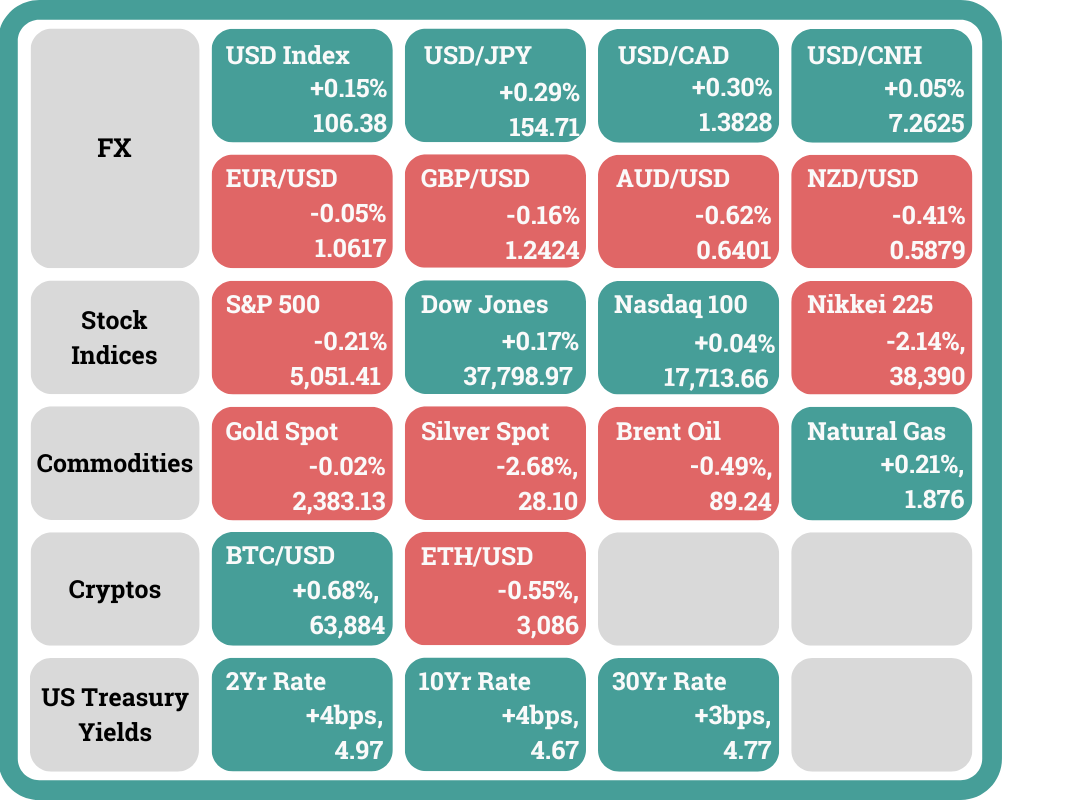

The US Treasury Yield curve inversion remained at 0.30% as the US 2-year bond yield and the 10-year yield rose +0.04% to 4.97% and 4.67% respectively.

The US stock futures traded within a small range through the Asian and London trading sessions. The S&P 500 futures was up merely +0.11% when the New York session began.

The US stock market opened almost unchanged from Monday. It then continued to trade in a larger range through the New York session and did not react strongly to Powell delaying his expectation for the first interest rate cut (headline 1). The S&P 500 finished -0.21% lower (high: +0.36%, low: -0.43%), the Dow Jones rose +0.17% (high: +0.68%, low: -0.06%) while the Nasdaq edged +0.04% higher (high: +0.63%, low: -0.26%).

The crypto market tried to go lower with Bitcoin testing the 61,700 range multiple times, falling as low as 61,709 (-2.8%) intraday. Ether tested the 3,000 as well, falling as low as 2994 (-3.5%) intraday.

Headlines & Market Impact

Fed Chair Powell says there has been a ‘lack of further progress’ this year on inflation

Notable Snippet: Federal Reserve Chair Jerome Powell said Tuesday that the U.S. economy, while otherwise strong, has not seen inflation come back to the central bank’s goal, pointing to the further unlikelihood that interest rate cuts are in the offing anytime soon.

Speaking to a policy forum focused on U.S.-Canada economic relations, Powell said that while inflation continues to make its way lower, it hasn’t moved quickly enough, and the current state of policy should remain intact.

“More recent data shows solid growth and continued strength in the labour market, but also a lack of further progress so far this year on returning to our 2% inflation goal,” the Fed chief said during a panel talk.

Echoing recent statements by central bank officials, Powell indicated the current level of policy likely will stay in place until inflation gets closer to target.

“The recent data have clearly not given us greater confidence, and instead indicate that it’s likely to take longer than expected to achieve that confidence,” he said. “That said, we think policy is well positioned to handle the risks that we face.”

Powell added that until inflation shows more progress, “We can maintain the current level of restriction for as long as needed.”

“We’ve said at the [Federal Open Market Committee] that we’ll need greater confidence that inflation is moving sustainably towards 2% before [it will be] appropriate to ease policy,” he said.

What we think: Markets have been pricing in this new fact recently with dwindling odds of 3 interest rate cuts happening this year. However, if we should see new data coming forth to reverse the recent inflation trend, we may see an abrupt change in both risk sentiment and the Fed stances.

Lagarde says ECB will cut rates soon, barring any major surprises; notes ‘extremely attentive’ to oil

Notable Snippet: European Central Bank President Christine Lagarde on Tuesday said the central bank remains on course to cut interest rates in the near term, subject to any major shocks.

Lagarde said the ECB would monitor oil prices “very closely” amid elevated fears of a spillover conflict in the Middle East. However, since Iran’s unprecedented air attack on Israel over the weekend, she said the oil price reaction had been “relatively moderate.”

“We are observing a disinflationary process that is moving according to our expectations,” Lagarde told CNBC’s Sara Eisen on the sidelines of the IMF Spring Meetings.

“We just need to build a bit more confidence in this disinflationary process but if it moves according to our expectations, if we don’t have a major shock in development, we are heading towards a moment where we have to moderate the restrictive monetary policy,” Lagarde said.

“As I said, subject to no development of additional shock, it will be time to moderate the restrictive monetary policy in reasonably short order,” she added.

Asked whether a June rate cut might be followed by subsequent reductions, Lagarde replied, “I have been extremely clear on that and I have said deliberately we are not pre-committing to any rate path.”

“There is huge uncertainty out there. … We have to be attentive to those developments, we have to look at the data, we have to draw conclusions from those data.”

What we think: Lagarde continues to be vocal about the need for interest rates to be cut soon.

Japan firms business mood slips as weak yen squeezes households

Notable Snippet: Business confidence at big Japanese manufacturers and services sector firms slid in April from the prior month, dragged down by cost-of-living pressures and shaky economic conditions in major market China, a Reuters monthly poll showed.

The yen's weakening to levels unseen since 1990 during the heyday of the asset-inflated bubble is lifting the cost of imports in a blow to household consumption, according to the Reuters Tankan survey.

Moreover, while the fall in currency has boosted the value of exports, volume of shipments have not benefited as much, the survey found.

The Reuters Tankan sentiment index for manufacturers stood at plus 9, down from the previous month's 10, dragged down by chemicals and food processing.

The services sector index fell to plus 25 from plus 32 in the previous month, despite some gains by retailers. The survey, conducted April 3-12, found that both sectors' sentiment indexes improved slightly over the coming three months.

The monthly Reuters Tankan, which closely tracks the Bank of Japan's quarterly tankan survey, was conducted during the time the Japanese currency hit its 34-year lows to the dollar beyond 153 yen. That has prompted repeated warnings from authorities that they stood ready to take action against speculative or destabilising currency moves. The dollar broke above 154 yen this week.

"Our sales appear to be boosted due to the impact of a weak yen, but there's no sign of recovery in terms of volume," a manager of a chemicals maker wrote in the survey on condition of anonymity.

On top of the fragile domestic demand, external factors were also cited as a source of concern for Japanese firms.

What we think: The policymakers in Japan may be pressured to act on the weak Yen soon, especially since the weak Yen is eroding the purchasing power of the average Japanese consumer and eating at the revenue of Japanese businesses.

Sentiment

FX

Stock Indices

Best,

Phan Vee Leung

CIO & Founder, TrackRecord